The New Populism Needs to Get This Straight (about budget surpluses)

New Economic Perspectives has the article The New Populism Needs to Get This Straight by Joe Firestone. Until very recently, I would have been shocked by what this article has to say.

…the economic fact that the surpluses of the Clinton’s term, as well as his deficit reduction policies, were bad for the US because they reduced or eliminated private sector surpluses causing a growth in private sector debt in Clinton’s “goldilocks” economy.

.

.

.

It would greatly help the new populism and the DC progressive establishment, also, if it took the trouble to learn a simple macroeconomic equation, which is an accounting identity, and which will help them gain clarity of thinking when it comes to fiscal policy, trade policy, and their inter-relationship. That equation is:The Government Sector Balance + The Private Sector Balance + The Foreign Sector Balance = 0; where the balances refer to transaction flows in an accounting period.

The Government Sector Balance is positive when the Government taxes more dollars than it spends. That’s what we’ve been calling “a surplus.” The private sector is positive when it saves more dollars than it spends, and the foreign sector is positive when it saves more dollars than it spends. This last, please note, is equivalent to what I’ve been calling a “trade deficit.”

So now, let’s say people want to save 6% of GDP per year, and they also want to run a trade deficit of 4% of GDP per year. Then a policy of deficit reduction that aims at a deficit of 3% obviously won’t accommodate these private sector desires, since 6% + 4% requires a government deficit of 10% for support.

The point of this article is that you may be surprised at who goes into debt when the government runs a surplus as opposed to who goes into debt when it is just a question of very unequal distribution of wealth. When you put together insufficient deficit and very unequal distribution of wealth, you get the great recession of 2008-2010 and the still present aftermath.

Until I started reading New Economic Perspectives and reading about MMT in other places as well, I depended on my knowledge of economics from what I learned in the early 1960s. I was and am a firm believer in Keynesian economics. However, I did not understand the debt and deficit the way I do now as explained in this article.

The people who blog in places like New Economic Perspectives need to understand that even their potential allies, who escaped the brainwashing of the Kochs and of Pete Peterson, may still have trouble understanding the impact of deficits and surpluses as now so well understood by people who are current.

So keeping up the efforts to re-educate and specifically communicating with progressives is essential to shifting the country’s thinking.

Extra credit diversion.

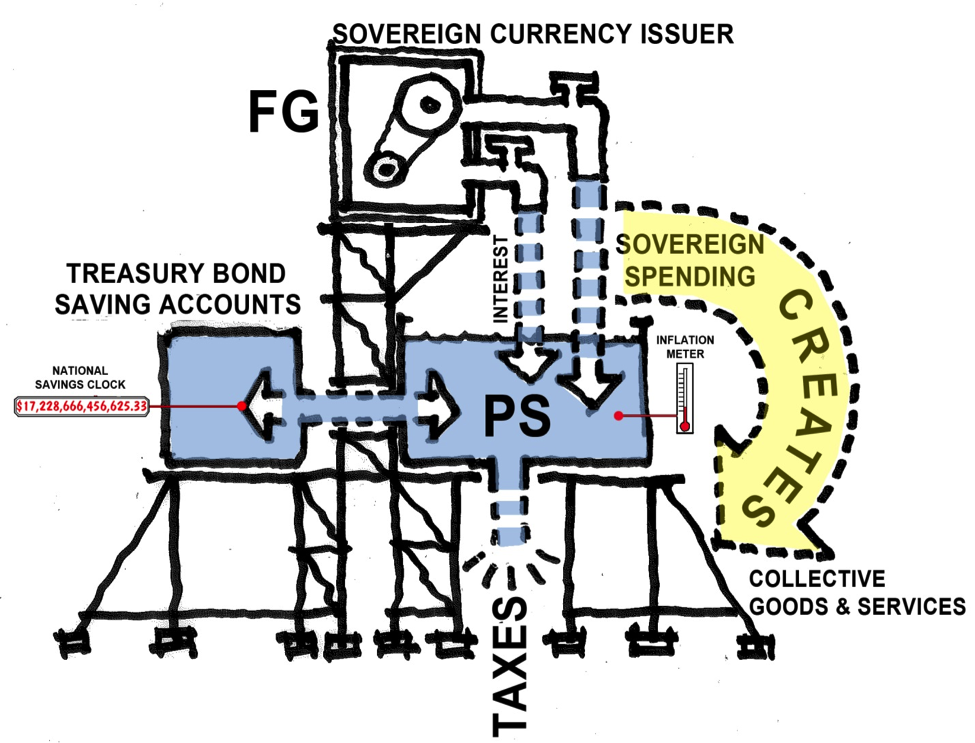

It is interesting to reconcile these ideas with the ideas from my previous post Diagrams and Dollars: Modern Money Illustrated (Part 1 & 2). Let us look at the final diagram from that post.

The PS pot is for the “Private Sector”, and the FG pot is for the “Federal Government”. The issue of Private Sector debt is hidden by this diagram because the PS pot is undifferentiated. To really understand the point of the current article, you have to see that the PS pot can be separated into the domestic private sector and foreign part of the “private” sector. The “foreign sector balance” in the equation from the current article [which has nothing to do with the FG pot] is the part of the PS pot that is not domestic. The “private sector balance” in the equation from the current article is the “domestic part” of the PS pot.

The level of the Treasury Bond Saving Accounts pot is labeled “National Savings Clock”. I think this is a misnomer. This total is for the entire savings from the PS pot which includes non-domestic savings in USA money. Also realize that the contents of the Treasury Bond Saving Accounts pot is held by the FG where it is accounted for as as a liability just like a savings account sitting in a bank is thought of as a liability of the bank.

Also note that the domestic part of the PS pot can be further divided into the part for the wealthy 1% of the domestic population and the part for the other 99% of the population. A lot of our troubles are hidden in that separation.

The totals for the PS pot may look great, but the health of the different parts of that pot may look totally different from the pot as a whole.

This discussion is already getting too complicated. I really need to make my own drawing and devote a separate article to this topic.

There is a link above to the book Modern Money Theory: A Primer on Macroeconomics for Sovereign Monetary Systems [Paperback] by L. Randall Wray.